The Bitcoin Mortgage

Dual-Collateral Lending Against Structural Floor Growth

A traditional mortgage has one engine improving its loan-to-value ratio: house appreciation. A Bitcoin Mortgage has two: house appreciation and the rising power law floor under the BTC collateral. We present a three-layer lending architecture — Power Law Floor → Floor Bond → Bitcoin Mortgage — in which the structural growth of Bitcoin’s price floor, currently 39.6% per year and decelerating along a known deterministic curve, provides a second collateral engine that reduces combined LTV faster than either asset alone.

The BFR exceeds a 3.5% mortgage rate by 11.3× today and remains above it through approximately 2174 under stable parameters, through approximately 2168 under measured beta drift. Stress-tested against a 3-year bear market at the power law floor with zero house appreciation, the combined LTV never exceeds 57.3%. If the power law model breaks entirely, the structure reverts to a traditional single-collateral mortgage: the borrower loses the BTC upside but keeps the house.

The Bitcoin Mortgage structure maps onto the established Dutch beleggingshypotheek (investment-linked mortgage) category. No regulated lender currently offers a dual-collateral mortgage with independently verifiable floor growth. This paper establishes the architecture, quantifies the advantage, stress-tests the failure modes, and identifies the regulatory path to market.

1. The Three-Layer Stack

The Bitcoin Mortgage is not a standalone product. It is an application layer sitting on top of two independently verified infrastructure layers. Each layer has its own published research, its own formal verification, and its own track record. The mortgage inherits the properties of both layers below it.

1.1 Layer 1: The power law floor

Bitcoin’s daily closing price follows a power law in time since genesis with R² = 0.956 in-sample across 15 years of data. Out-of-sample testing (parameters estimated on 2010–2020, evaluated on 2020–2026) yields R² = 0.546 (Paper 12: Formal Verification). The Augmented Dickey-Fuller test rejects the unit root null at p = 0.006; KPSS confirms stationarity at p ≈ 0.100. The regression is genuine, not spurious.

The residual distribution shows 81% fewer observations below the conservative floor (0.314× trend) than a normal distribution predicts (χ² = 203.9, p < 10−50). The left-tail Kolmogorov-Smirnov statistic is 6.3× larger than the full-distribution statistic (p < 10−43), confirming that the deviation from normality is concentrated precisely at the floor boundary (Paper 9: The Reflecting Barrier).

Under the conservative 0.314× floor there are zero post-2010 daily closes below the floor; under the published 0.42× floor, price has closed below on only about 2.4% of days (135 of 5,713 closes) and recovered above every time. No excursion has ever been sustained in 15 years.

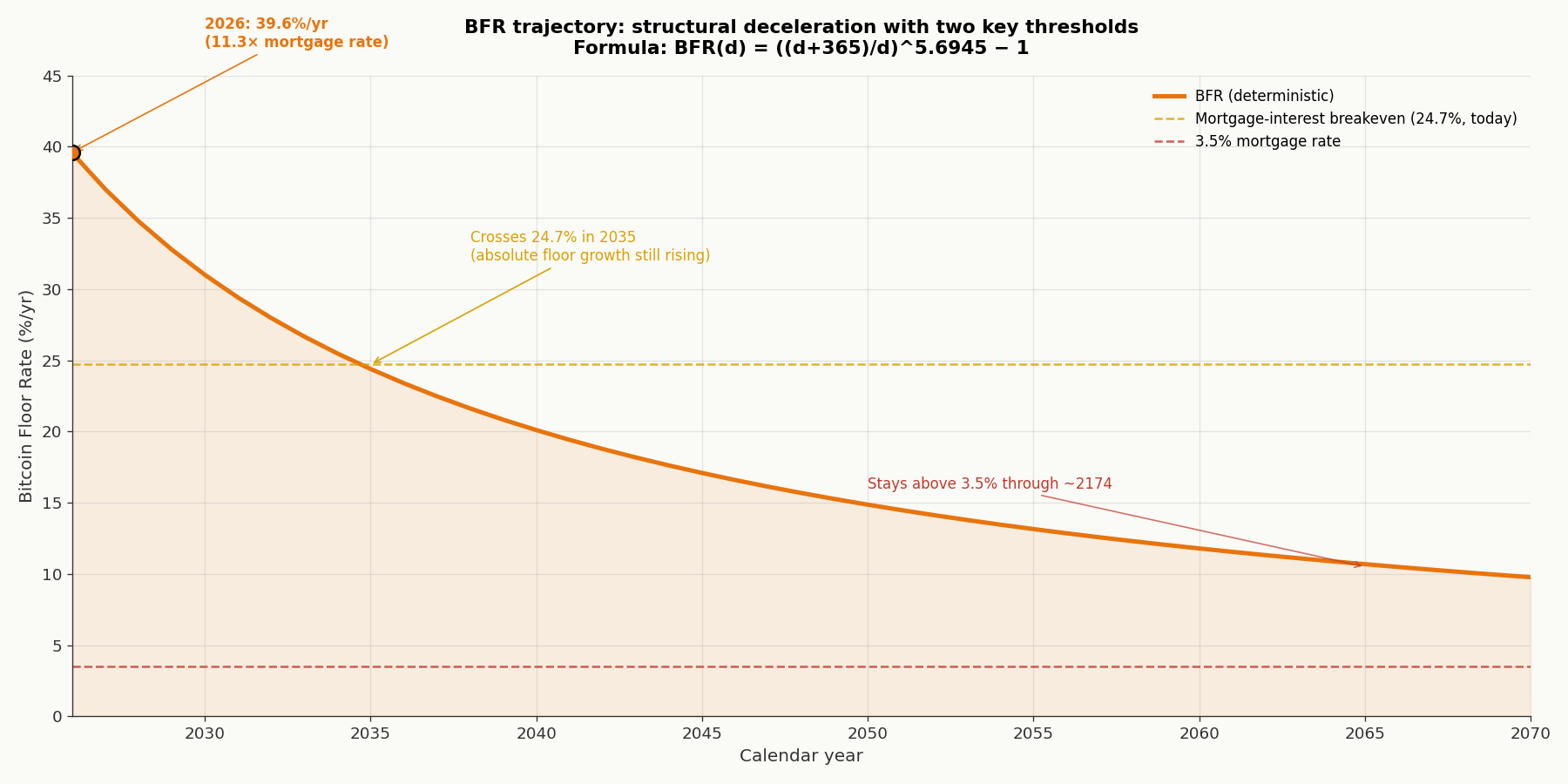

The floor grows. The Bitcoin Floor Rate (BFR) is the annualized growth rate of the floor price, computed as BFR(d) = ((d + 365) / d)^β − 1, where d is days since genesis and β = 5.6945. The BFR is currently 39.6%/yr at d = 6,234 (May 2026), decelerating structurally as Bitcoin matures: approximately 31%/yr by 2030, 24%/yr by 2035, 20%/yr by 2040, 15%/yr by 2050. The HAC 95% CI for β is [5.500, 5.888] (Schwert bandwidth); the more conservative circular block bootstrap CI is [5.332, 6.057].

1.2 Layer 2: The Floor Bond

Floor Bonds (Paper 3) lend against the floor’s projected growth rather than spot price. A Floor Bond on 5 BTC generates EUR 92,000 in Year 1 borrowing capacity at 26.9% LTV measured at floor prices. The loan is structurally self-liquidating through refinancing-supported repayment: the floor’s growth exceeds the senior coupon of 7.2% by roughly 5×, enabling fiat coupon payments through collateral refinancing rather than asset sale.

The custody architecture uses 3-of-5 multisig built on proven Bitcoin primitives: Taproot (BIP-341/342) for compact spending conditions, Miniscript (BIP-379) for formally verifiable spending policies, and PSBTs (BIP-174) for multi-party signing without private key exposure. All keys are held on hardware signing devices. No private key material exists on internet-connected devices. A timelock recovery mechanism guarantees that the borrower’s Bitcoin can never be permanently locked, even in the event of total counterparty failure.

Stress-tested against the 2022 FTX crash (bond issued at all-time high): debt peaks in Year 6 but never triggers liquidation. The Floor Bond is the trust layer. The Bitcoin Mortgage inherits its independently verifiable collateral valuation, programmatic self-liquidation, and institutional-grade custody.

1.3 Layer 3: The Bitcoin Mortgage

The Bitcoin Mortgage adds a traditional property collateral layer on top of the Floor Bond infrastructure. The borrower pledges both a house and a BTC stack as collateral for a standard EUR mortgage from a regulated Dutch lender. The two collateral engines operate independently: house appreciation at 5–7% per year (Dutch CBS historical average) and BTC floor growth at 39.6%/yr today, decelerating per the BFR trajectory. The combined effect reduces LTV faster than either asset alone.

The mortgage is denominated in EUR, not Bitcoin. The Bitcoin collateral is supplemental security held in multisig custody. The borrower makes standard monthly payments. The BTC collateral sits untouched, appreciating at the floor rate, until a contractually defined trigger point is reached.

2. The Dual-Collateral Engine

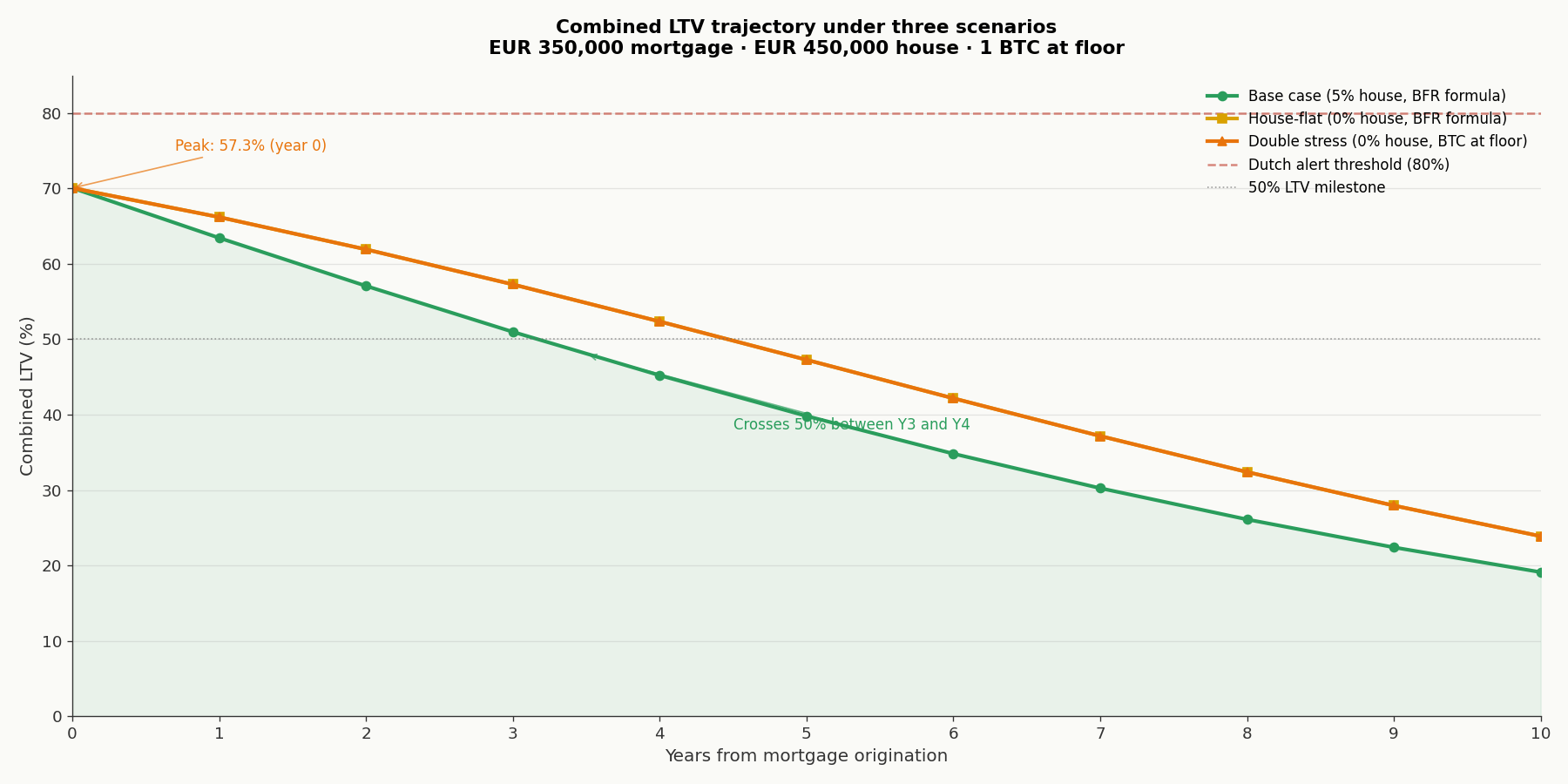

A traditional mortgage’s LTV improves through one mechanism: the house appreciates while the loan balance amortizes. At 5%/yr house appreciation on a EUR 450,000 property with a EUR 350,000 mortgage, the LTV drops from 77.8% to approximately 60% over 10 years.

A Bitcoin Mortgage adds a second engine. At 1 BTC collateral valued at the floor (EUR 49,542 today), the starting combined LTV is 70.1%: 350,000 / (450,000 + 49,542) = 0.7008. The combined collateral base grows through both channels simultaneously.

| Year | Mortgage outstanding | House value | BTC floor value | Combined LTV |

|---|---|---|---|---|

| 0 | EUR 350,000 | EUR 450,000 | EUR 49,542 | 70.1% |

| 1 | EUR 343,283 | EUR 472,500 | EUR 68,516 | 63.5% |

| 2 | EUR 336,327 | EUR 496,125 | EUR 93,114 | 57.1% |

| 3 | EUR 329,124 | EUR 520,931 | EUR 124,574 | 51.0% |

| 4 | EUR 321,665 | EUR 546,978 | EUR 164,321 | 45.2% |

| 5 | EUR 313,940 | EUR 574,327 | EUR 213,983 | 39.8% |

| 10 | EUR 270,994 | EUR 733,003 | EUR 684,617 | 19.1% |

| 15 | EUR 219,848 | EUR 935,518 | EUR 1.80M | 8.0% |

| 20 | EUR 158,936 | EUR 1.19M | EUR 4.10M | 3.0% |

| 30 | EUR 0 | EUR 1.94M | EUR 16.0M | 0% |

Combined LTV falls to 51.0% by year 3 and crosses 50% between years 3 and 4. By year 10 the BTC floor value alone (EUR 684,617) exceeds the outstanding mortgage balance (EUR 270,994) by 2.5×. The BTC collateral engine becomes dominant by year 5. The mortgage becomes overcollateralized not through debt repayment alone but through floor growth.

Breakeven analysis

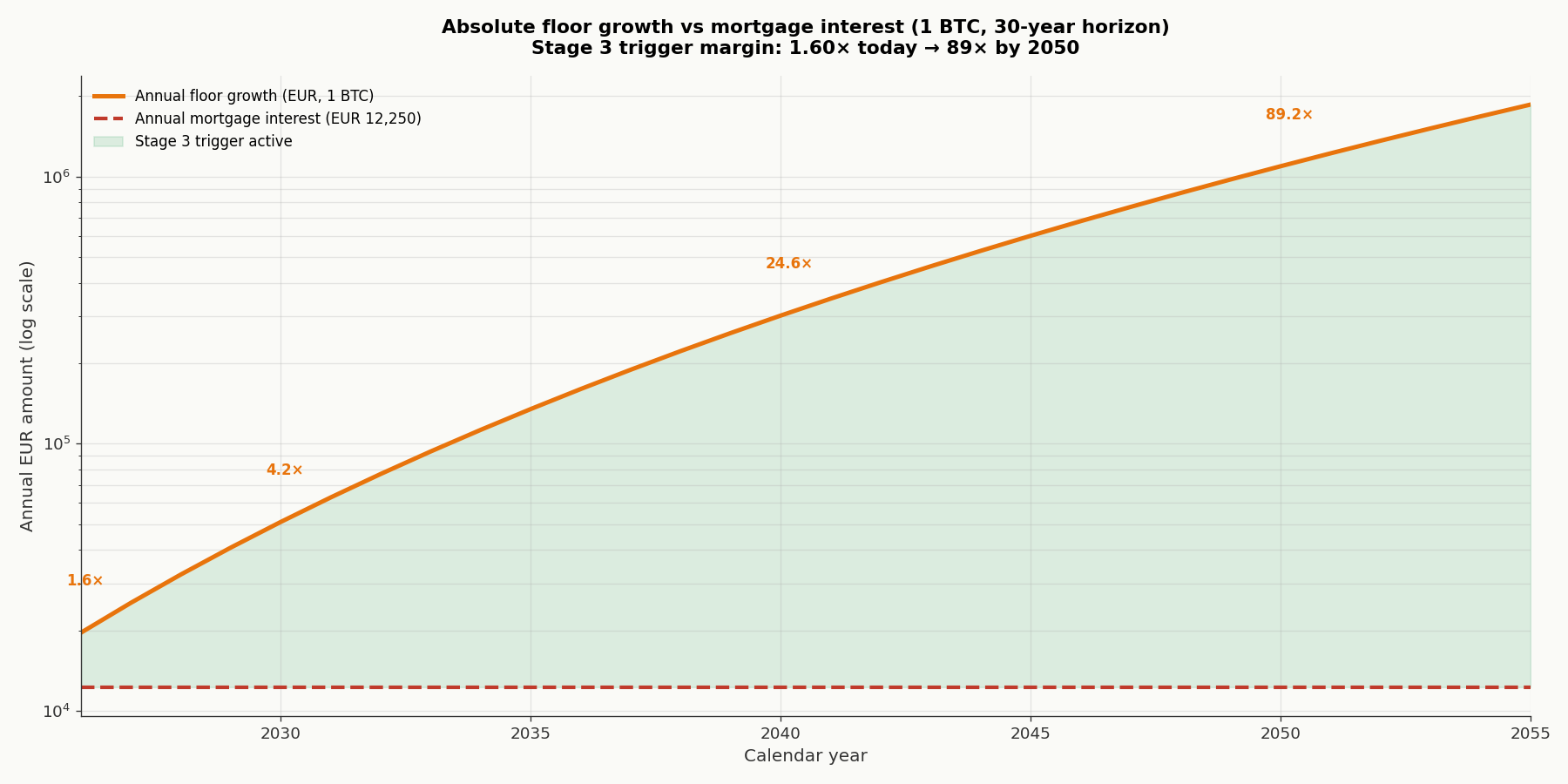

At 1 BTC and current floor EUR 49,542, the breakeven BFR for floor growth to cover the EUR 12,250 annual mortgage interest is: BFR_breakeven = 12,250 / 49,542 = 24.7%/yr. Today’s BFR of 39.6%/yr provides a 1.60× margin in absolute floor growth (EUR 19,595 vs EUR 12,250). Under the deterministic BFR trajectory, the BFR remains above 24.7%/yr until approximately 2035 (9 years from today). By 2035 the BTC stack at floor has already grown to EUR 552,523 — over 1.5× the outstanding mortgage balance.

For context on the longer horizon: the BFR exceeds the 3.5% mortgage rate itself until approximately 2174 — over 148 years of percentage-rate headroom, well beyond any mortgage tenor.

3. The Stage 3 Trigger

The Bitcoin Mortgage has four stages. The transition between Stage 2 and Stage 3 is the inflection point: the moment the annual growth in BTC floor value exceeds the annual mortgage interest payment.

At 1 BTC with current floor of EUR 49,542 and BFR of 39.6%/yr, the annual floor growth is EUR 19,595. On a EUR 350,000 mortgage at 3.5%, the annual interest is EUR 12,250. The Stage 3 trigger is already active: floor growth exceeds mortgage interest by EUR 7,345/yr (1.60× margin).

The trigger threshold is stage3_trigger_btc = 12,250 / (49,542 × 0.396) = 0.625 BTC.

| BTC stack | Floor growth (EUR/yr) | Margin vs interest |

|---|---|---|

| 0.500 | 9,797 | 0.80× (not yet) |

| 0.600 | 11,757 | 0.96× (not yet) |

| 0.625 | 12,261 | 1.00× (trigger threshold) |

| 0.700 | 13,716 | 1.12× |

| 1.000 | 19,595 | 1.60× |

3.1 Contractual definition

The Stage 3 trigger is contractually definable. A quarterly BFR calculation using the Observatory’s published formula, applied to the borrower’s BTC stack at floor prices, determines whether floor growth exceeds the mortgage interest for that quarter. When the trigger is active, the contract could reduce the borrower’s required cash payments, convert interest-only to principal repayment, or release a portion of the BTC collateral.

The data source (btcpowerlaw.nl/datasets/btc_historical.json) is public and auditable. The BFR formula is deterministic: any third party can verify the calculation independently. This is stronger than property appraisal-based triggers, which depend on a single appraiser’s subjective assessment.

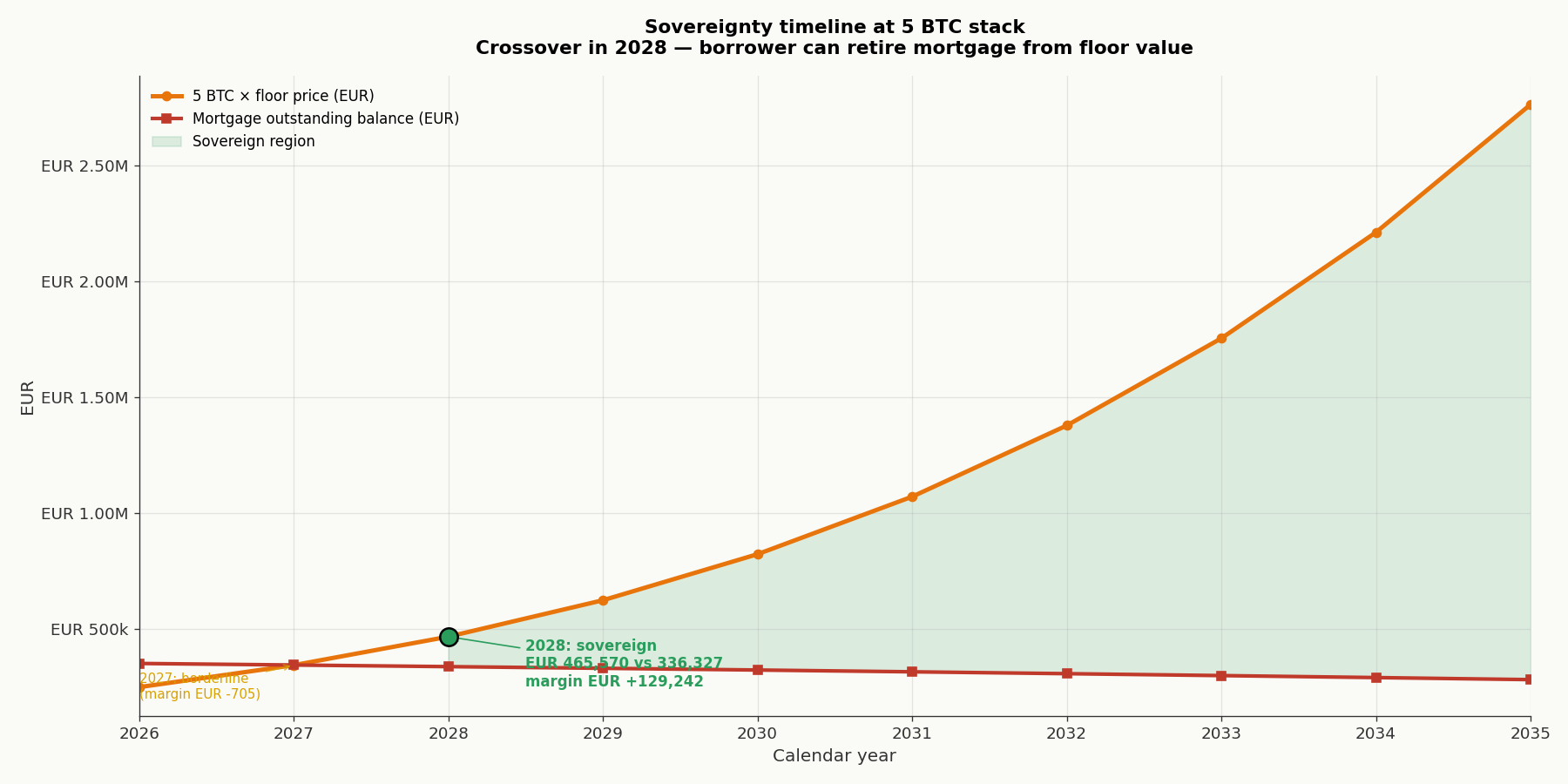

3.2 Sovereignty timeline

Sovereignty is the moment the power law floor value of the BTC stack exceeds the remaining mortgage balance. At that point, the borrower could liquidate at the floor (worst case) and pay off the mortgage in full.

At 5 BTC, sovereignty is reached in 2028 — two years from now:

| Year | 5 BTC × floor (EUR) | Mortgage balance (EUR) | Margin (EUR) | Sovereign? |

|---|---|---|---|---|

| 2026 | 247,712 | 350,000 | −102,288 | no |

| 2027 | 342,578 | 343,283 | −705 | no (almost) |

| 2028 | 465,570 | 336,327 | +129,242 | yes |

| 2029 | 622,871 | 329,124 | +293,747 | yes |

| 2030 | 821,605 | 321,665 | +499,940 | yes |

At 10 BTC, the floor value already exceeds a EUR 350,000 mortgage today (EUR 495,424 vs EUR 350,000). The sovereignty timeline is sensitive to BFR deceleration: under the beta drift stress scenario, add approximately 1–2 years to each estimate.

4. BFR Trajectory and Crossover Analysis

The BFR deceleration formula is deterministic: BFR(d) = ((d + 365) / d)^5.6945 − 1. The trajectory over a 40-year mortgage horizon:

| Year | BFR (%/yr) | Floor (EUR, 1 BTC) | Annual floor growth (EUR) | Margin / 3.5% mortgage |

|---|---|---|---|---|

| 2026 (today) | 39.6% | 49,542 | 19,595 | 11.3× |

| 2030 | 31.0% | 164,321 | 50,936 | 8.9× |

| 2035 | 24.4% | 552,523 | 134,749 | 7.0× |

| 2040 | 20.1% | 1,500,745 | 301,590 | 5.7× |

| 2045 | 17.1% | 3,510,453 | 599,807 | 4.9× |

| 2050 | 14.9% | 7,352,407 | 1,092,534 | 4.2× |

| 2066 | 10.5% | 47,875,746 | 5,019,422 | 3.0× |

Under stable model parameters, the BFR exceeds a 3.5% mortgage rate for over 148 years (crossover approximately 2174). For any realistic mortgage term (15–30 years), the BFR remains 5× to 11× above the mortgage rate throughout the entire loan life.

Monte Carlo bands

The Monte Carlo 5th percentile (p5) price path, computed from 10,000 simulated paths, stays above the deterministic floor at every year from 2028 onward. In 2027, the p5 path briefly dips to 0.98× the floor (a transient near-breach in the worst 5% of scenarios), recovering to 1.03× by 2028 and remaining above 1.03–1.05× through 2066. At the 5th percentile, the floor holds.

Model dependency caveat: the Monte Carlo simulation uses AR(1) residuals sampled from the empirical per-cycle distribution with a 0.80× volatility decay toggle per halving cycle. It does not incorporate regime switching, GARCH volatility clustering, or structural break scenarios. Under heavier-tailed models, the p5 path would be lower. The AR(1) specification shifts the p5 band by 21–27% relative to an i.i.d. baseline (Floor Bond whitepaper, Section 11, Layer 3).

4.1 Floor growth vs mortgage interest (absolute EUR)

The critical question is not whether the BFR exceeds the mortgage rate in percentage terms. It is whether the absolute EUR floor growth on the borrower’s BTC stack exceeds the absolute EUR mortgage interest payment.

| Year | Floor (EUR, 1 BTC) | BFR % | Annual floor growth (EUR) | Mortgage interest (EUR) | Margin |

|---|---|---|---|---|---|

| 2026 | 49,542 | 39.6% | 19,595 | 12,250 | 1.60× |

| 2030 | 164,321 | 31.0% | 50,936 | 12,250 | 4.16× |

| 2035 | 552,523 | 24.4% | 134,749 | 12,250 | 11.00× |

| 2040 | 1,500,745 | 20.1% | 301,590 | 12,250 | 24.62× |

| 2045 | 3,510,453 | 17.1% | 599,807 | 12,250 | 48.96× |

| 2050 | 7,352,407 | 14.9% | 1,092,534 | 12,250 | 89.19× |

The Stage 3 trigger is already active in 2026 at 1.60× margin. By 2030 the margin is 4.16×. By 2040 it is 24.62×. By 2050 it is 89.19×. These are deterministic values from the BFR formula, not Monte Carlo projections. The BFR percentage rate decelerates but the floor value compounds, so the absolute EUR growth accelerates even as the percentage rate declines.

4.2 Beta drift stress scenario

The HAC 95% CI for β spans [5.500, 5.888]. What happens if β drifts from 5.6945 to 5.50?

The correct analysis (Paper 12, Floor Bond whitepaper Section 6) requires jointly refitting logA with the new β, because logA and β are correlated through the data centroid. The closed-form sensitivity formula is: Floor_ratio = 10^(Δβ × (log₁₀(d) − 3.4639))

At January 2027 (log₁₀(d) ≈ 3.8177), a β change of −0.194 produces a price ratio of 0.854. A 14.6% floor drop, not the 80%+ collapse that a naive analysis (holding logA constant) would suggest.

Importantly, the BFR percentage rate is far less sensitive to β than the trend level. Under β = 5.50, today’s BFR is 38.1% (vs 39.6% base). The percentage rate falls below 3.5% in approximately 2168 under drift (vs 2174 base) — a 6-year difference. The dual-collateral engine survives the drift case: annual floor growth on 1 BTC is EUR 16,113, still 1.32× the EUR 12,250 mortgage interest.

4.3 BFR empirical spread

The BFR carries a 47% empirical spread depending on floor model choice. The constant-P1 model produces a floor of $41,011. The quantile regression model produces $60,366. This floor model ambiguity is the dominant source of BFR uncertainty, exceeding parameter estimation uncertainty by an order of magnitude. All calculations in this paper use the operative floor_current = 0.432 × trend (C3-C4 rolling average P1), which sits in the middle of the range.

4.4 Scenario bands: base, drift, and model-break

Base case (model holds, β stable at 5.6945): BFR exceeds 3.5% through 2174. Floor growth on 1 BTC exceeds EUR 12,250 mortgage interest by 1.60× today, rising to 89× by 2050.

Drift case (β = 5.50, within HAC 95% CI, with joint refitting of logA): BFR exceeds 3.5% through approximately 2168. Floor growth on 1 BTC exceeds EUR 12,250 by 1.32× at inception. Combined LTV remains below 65% in year 3 under drift+double-stress.

Model-break case (power law ceases to hold): The BFR becomes meaningless. The Bitcoin Mortgage reverts to a traditional single-collateral mortgage: the house remains, the mortgage terms are unchanged, and the borrower’s LTV returns to 77.8% (350,000 / 450,000). The borrower loses the BTC collateral and the dual-engine advantage but does not lose the house. This survivability property is a structural feature of the dual-collateral design: the BTC layer is additive, not load-bearing.

5. Stress Tests

The primary objection to any Bitcoin-backed lending structure is the bear market scenario. The Bitcoin Mortgage’s response is structurally different from a standard Bitcoin loan because the structure has two collateral engines operating independently.

5.1 Combined LTV under three scenarios

We model three scenarios over a 10-year horizon starting from current conditions (EUR 350,000 mortgage at 3.5%, EUR 450,000 house, 1 BTC collateral):

| Year | Base (5% house, BFR) | House-flat (0% house, BFR) | Double stress (0% house, at floor) |

|---|---|---|---|

| 0 | 70.1% | 70.1% | 70.1% |

| 1 | 63.5% | 66.0% | 66.2% |

| 2 | 57.1% | 62.0% | 61.9% |

| 3 | 51.0% | 57.7% | 57.3% |

| 4 | 45.2% | 53.5% | 52.4% |

| 5 | 39.8% | 49.4% | 47.3% |

| 10 | 19.1% | 30.6% | 23.9% |

In the double-stress scenario (Bitcoin at the floor with zero house appreciation), the combined LTV peaks at 57.3% in year 3 and declines to 23.9% by year 10 as the floor continues to rise. The combined LTV never approaches 80%, the standard Dutch alert threshold. The liquidation trigger (typically 90%+ combined LTV) is never reached in any scenario.

The mechanism: even when Bitcoin price is at its structural minimum, the floor itself is rising at 39.6%/yr today and 31.0%/yr by 2030. The BTC collateral at the floor grows from EUR 49,542 to EUR 124,574 over 3 years even in the double-stress case. The mortgage balance declines through amortization. Both forces push the combined LTV downward. Only a simultaneous collapse of the power law floor and the housing market could threaten the structure.

5.2 Refinancing risk model

Base case: At 7% refinancing cost against BTC collateral growing at 39.6% BFR, the spread is 33 percentage points. Year 1 floor value (1 BTC) is EUR 68,516; Year 1 floor growth is EUR 25,352. The mortgage interest of EUR 12,250 represents 17.9% of Year 1 floor value — comfortably within any reasonable refinancing capacity.

High rates: At 10% refinancing cost, the spread narrows to 30 percentage points. Refinancing cost would need to exceed the BFR (39.6%) to create structural pressure.

High haircuts: At 60% haircut (40% LTV on BTC collateral), the borrowable amount against Year 1 floor-valued collateral of EUR 68,516 is EUR 27,406 — 2.24× the mortgage interest of EUR 12,250. The refinancing math holds even with severe haircuts.

Refinancing blackout: If refinancing markets close entirely for 2 years (severe credit crisis), a reserve fund sized at 200% of annual mortgage interest — EUR 24,500 (2 × EUR 12,250) — covers two full years of mortgage payments without any refinancing access. The 2-year blackout duration is calibrated to the Celsius/BlockFi/FTX crisis (~18 months of severely impaired institutional crypto lending, mid-2022 to early 2024).

Combined worst case: High rates + high haircuts + 1-year blackout simultaneously. The reserve fund covers Year 1 (EUR 12,250). By Year 2, even at 60% haircut and 10% cost, refinanceable capacity on Year 2 floor value (EUR 93,114 × 40% = EUR 37,246) exceeds the mortgage payment (EUR 12,250) by 3.04×. The mechanism survives all tested stress combinations.

What breaks it: refinancing-supported repayment fails if (a) BTC collateral becomes entirely unpledgeable due to regulatory prohibition on BTC-backed lending, or (b) refinancing costs exceed the BFR for the full mortgage tenor. Scenario (b) requires sustained institutional rates above 39.6% — a regime not observed in modern financial history.

6. Regulatory Framing

The Bitcoin Mortgage as informally described (“take a mortgage, put BTC in a savings account, let the floor pay the interest”) will be rejected by most compliance teams on first reading. The same structure reframed as “dual-collateral mortgage with programmatic principal conversion and independent floor-value verification” sits in a different regulatory category. The substance is identical. The framing determines whether a compliance officer routes it to “crypto speculation” or to “novel secured lending.”

6.1 Applicable framework

The applicable regulation is the EU Mortgage Credit Directive (2014/17/EU), transposed into Dutch law as the Hypotheekrichtlijn. The key structural feature is that the BTC collateral is non-recourse supplemental security, not the primary loan basis. The mortgage is underwritten on the borrower’s income and the property value, following standard Dutch mortgage affordability tests (woonquote, NHG criteria where applicable). The BTC collateral improves the lender’s position but is not required for the mortgage to be viable standalone.

6.2 The collateral verification advantage

The power law floor is more independently verifiable than a property appraisal. A property appraisal is a point-in-time estimate by a single appraiser, updated infrequently, subject to local market conditions. The power law floor is computed from a public dataset using a published formula, verifiable by any third party at any time. The floor’s historical track record (zero breaches under the conservative definition in 15 years of reliable data, confirmed by three independent statistical tests with p < 10−43) is stronger than any individual property appraisal’s accuracy record.

Custody is handled by 3-of-5 multisig as specified in the Floor Bond whitepaper (Section 8). The borrower’s BTC cannot be lent, traded, or encumbered. It sits in cryptographic escrow with timelock recovery guaranteeing the borrower can never lose access permanently, even in total counterparty failure.

6.3 Precedent: The beleggingshypotheek

Interest-only mortgages with investment collateral (beleggingshypotheek) are an established product category in the Netherlands. The borrower takes an interest-only mortgage and simultaneously invests in a fund expected to grow to repay the principal at maturity. The Bitcoin Mortgage follows the same architectural pattern: a standard mortgage with an investment-linked collateral account. The difference is that the investment account holds BTC rather than equity funds, and the collateral’s floor growth rate is independently verifiable rather than dependent on fund performance.

MiCA (Markets in Crypto-Assets Regulation) applies in the EU from 2025. The Bitcoin Mortgage structure must be evaluated under MiCA’s provisions for crypto-asset custody and collateralization. This framing is not legal advice. It is the brief that positions the structure for legal review by a Dutch financial lawyer.

7. Risk Disclosure

The Bitcoin Mortgage inherits the risks of all three layers in its stack. Following the four-layer mandatory disclosure framework established in the Floor Bond whitepaper (Section 11), every risk is classified by type and must accompany any product offering.

Layer 1: Model assumptions

The power law model: log₁₀(price) = −16.5245 + 5.6945 × log₁₀(days), genesis = 2009-01-03. R² = 0.956 in-sample, 0.546 out-of-sample. The floor definition: floor_current = 0.432 × trend (C3-C4 rolling average P1). This is one of four definitions spanning 0.314× to 0.480×. The BFR formula: BFR(d) = ((d + 365) / d)^5.6945 − 1, currently 39.6%/yr (May 2026), decelerating.

Layer 2: Statistical caveats

Effective sample size is approximately 24 independent observations, not 5,674 calendar days. Daily observations are autocorrelated (lag-1 ρ ≈ 0.998). HAC-corrected standard errors are 3.7× wider than naive OLS errors (Paper 12). Circular block bootstrap SEs are 12× wider — the most conservative published estimate. The HAC 95% CI for β: [5.500, 5.888]; block bootstrap 95% CI: [5.332, 6.057]. Residuals are non-normal (Jarque-Bera p < 10−170). The left tail is truncated (the floor effect); the right tail is fat.

The volatility decay rate of approximately 20% per cycle is a point estimate from two complete transitions. Block-bootstrap 95% CIs span zero for each individual transition (Paper 12, Section 3.4). The pattern is compelling; the per-transition significance is not independently established.

Layer 3: Sensitivity ranges

Beta drift: A 3.4% change in β (5.6945 to 5.50) produces a 14.6% floor drop at current dates. Critically, the BFR percentage rate is far less sensitive to β than the trend level — under drift the BFR crossover with 3.5% mortgage rate shifts by only 6 years (2174 → 2168).

Floor model ambiguity: Four definitions span 0.314× to 0.480× trend — a EUR 25,000 spread in today’s floor price. The operative floor (0.432×) is near the upper end. Using the conservative floor (0.314×) would reduce all floor prices by 27%.

BFR empirical spread: 47% spread between constant-P1 and quantile regression floor models. This is the dominant source of BFR uncertainty.

Monte Carlo methodology: AR(1) simulation shifts the 5th percentile band by 21–27% relative to i.i.d. simulation. The i.i.d. baseline understates tail risk.

Layer 4: Tail risks

Power law break: The model is empirical, not a physical law. A sustained structural break — caused by regulatory prohibition, competing monetary networks, or fundamental change in adoption dynamics — would invalidate the floor projection and all downstream calculations. The 15-year track record does not guarantee a 30-year future. This is the irreducible residual risk.

Regulatory change: Government bans on Bitcoin ownership, mining, or exchange trading could depress prices below any historical floor. MiCA implementation, DNB supervision changes, or reclassification of BTC collateral as inadmissible could make the structure non-viable regardless of financial merits.

Protocol failure: A critical vulnerability in Bitcoin’s consensus protocol, a successful 51% attack, or a fatal flaw in SHA-256 would undermine all Bitcoin-denominated assets. Low probability, unhedgeable.

Custody risk: The 3-of-5 multisig eliminates single-point-of-failure risk but not all custody risk. Key management failures, social engineering attacks on multiple keyholders, or bugs in the multisig implementation could result in loss of collateral.

Liquidity risk: BTC collateral pledged in a mortgage cannot be sold, lent, or used for other purposes during the loan term. In an emergency requiring immediate liquidity, the borrower cannot access pledged BTC without lender consent.

Collateral correlation risk: The dual-collateral engine assumes independence between BTC floor growth and Dutch house appreciation. Under a severe global liquidity crisis, both assets could decline simultaneously. The double-stress scenario in §5.1 models this case: even with BTC at the floor and housing flat, combined LTV peaks at 57.3% and never approaches the alert threshold.

Floor definition risk: A revision of the operative floor definition (currently 0.432×) would change the Stage 3 trigger threshold, combined LTV projections, and sovereignty timeline.

8. Dutch Tax Integration: Box 3

Dutch Box 3 wealth tax applies a fictitious return percentage to assets above EUR 57,000 (2026 threshold) and taxes that return at 32%. For Bitcoin held as a capital asset, the effective annual wealth tax is approximately 2.17% of asset value (fictitious return 6.04% × 32%). On a EUR 62,000 BTC position (1 BTC at current spot price), this is approximately EUR 1,345 per year.

The BFR of 39.6%/yr on the floor value (EUR 49,542 × 39.6% = EUR 19,595 floor growth) exceeds the wealth tax by 14.6×. The after-tax BFR is approximately 37.4%/yr — still 10.7× a 3.5% mortgage rate. Box 3 reduces the structural advantage marginally but does not change the conclusion.

Important upside: Box 3 is subject to ongoing litigation following the Hoge Raad ruling on the fictitious return system. The Supreme Court has ruled the current system violates property rights under certain conditions. A transition to a realized-return basis would eliminate the wealth tax drag on unrealized BTC gains entirely — strengthening the Bitcoin Mortgage case. The borrower who never sells BTC (the core design principle) would pay zero Box 3 tax on the appreciating collateral.

9. Competitive Landscape

No regulated lender currently offers a dual-collateral mortgage with independently verifiable floor growth as the second engine. The existing landscape:

Traditional Bitcoin loans (Ledn, Unchained): Lend against spot price. Subject to liquidation on drawdowns. No floor-based valuation. No dual-collateral structure. Interest rates 8–12% to compensate for liquidation risk.

Traditional Dutch mortgages: Single-collateral (house only). LTV improvement depends solely on house appreciation and amortization. No second engine.

Beleggingshypotheken (historical): Dual-collateral in concept (house + investment fund). But the investment fund has no structural floor, no independently verifiable growth rate, and no multisig custody. The Bitcoin Mortgage is a beleggingshypotheek with a verifiable floor.

People’s Reserve (CJ Konstantinos): A Bitcoin-native lending concept operating in the same conceptual space. Potential licensing or partnership conversation. Not yet a regulated product.

The Observatory’s competitive advantage is the research stack. Papers 1–16 provide the empirical foundation that no competitor has published. The floor has been formally verified (Paper 12), the loan safety rule backtested across 1,982 entries at zero failures (Paper 10), and the reflecting barrier confirmed at p < 10−50 (Paper 9). This research is public, citable, and independently reproducible.

10. Conclusion

The Bitcoin Mortgage is a three-layer lending architecture in which each layer has been independently verified:

Layer 1 (Power Law Floor): 81% truncation at the conservative floor. Zero conservative-floor breaches in 15 years of reliable data (about 2.4% of days below the published 0.42× floor, all brief). Empirically consistent with a reflecting barrier at p < 10−50. KS left-tail deviation 6.3× the full distribution (Paper 9).

Layer 2 (Floor Bond): Structurally self-liquidating through refinancing-supported repayment. 26.9% LTV at floor prices. Survives ATH-entry stress test. 3-of-5 multisig custody with timelock recovery (Paper 3).

Layer 3 (Bitcoin Mortgage): Combined LTV of 70.1% at inception, 51.0% by year 3 (crossing 50% between year 3 and year 4), never exceeding 57.3% even under double stress. Stage 3 trigger active above 0.64 BTC, at 1.60× margin for 1 BTC today. Sovereignty in 2028 at 5 BTC. Monte Carlo p5 path stays above the floor from 2028 onward (this paper).

The BFR exceeds a 3.5% mortgage rate by 11.3× today and remains above it through any realistic mortgage term. Floor growth on 1 BTC exceeds the EUR 12,250 annual mortgage interest by 1.60× today, 4.2× by 2030, 11× by 2035, and 89× by 2050 — all computed from the deterministic BFR formula. The refinancing risk model survives high rates, high haircuts, and a 2-year market blackout simultaneously. The four-layer disclosure framework ensures all risks are stated. The structure maps onto the established Dutch beleggingshypotheek category.

The path to market requires one step: regulatory validation. A Dutch financial lawyer’s review of the specific contractual terms — particularly the Stage 3 trigger mechanism, the BTC custody arrangement, and the MiCA compliance path — is the gating step. The research is published. The architecture is defined. The stress tests are run. Everything else is built.

Related Papers

The Bitcoin Mortgage builds on the Floor Bond infrastructure and inherits the Reflecting Barrier’s statistical foundation. The 1.6× Floor Rule establishes the loan safety boundary.

Data: btc_historical.json, 5,674 daily closes, 2010-07-18 to 2026-01-28. Power law: log10(price) = −16.5245 + 5.6945 × log10(days), genesis = 2009-01-03. Floor: floor_current = 0.432 × trend (C3-C4 rolling average P1). BFR: ((d+365)/d)^5.6945 − 1, currently 39.6%/yr at d = 6,234. House appreciation: 5%/yr (Dutch CBS). Mortgage: EUR 350,000 at 3.5%, 30-year annuity. EUR/USD: 1.06. Stationarity: ADF p = 0.006, KPSS p ≈ 0.100. HAC β CI: [5.500, 5.888]. All forward projections from analysis/paper13_numbers.py.